Dec 132017

| This program will figure many differnt types of financial calaculations. Includes loan payment schedules. | |||

|---|---|---|---|

| File Name | File Size | Zip Size | Zip Type |

| FINANCE.COM | 28952 | 18216 | deflated |

| FINANCE.DOC | 12307 | 4546 | deflated |

| FINANCE2.COM | 22064 | 14650 | deflated |

Download File FINANKT.ZIP Here

Contents of the FINANCE.DOC file

DOCUMENTATION FOR THE FINANCE I & FINANCE II ROUTINES

The routines in this program are all self prompting. When the main

menu is visible, just select the routine that you want to run by entering

the letter shown next to the routine. You will then see a new screen that is

waiting for your input. Enter the information that is being requested, then

press ENTER. You will be prompted for more information. When you are no

longer being prompted for information, the program will calculate and

display the results.

When you enter values you may use commas and dollar signs. DO NOT use

a percent sign or a cent sign. If you do so, the progam will not accept the

input and an error message will indicate that you did not enter a number.

The progam will then wait for you to reenter the information.

Remember, all interest rates are expressed in an annualized figure.

Periods per year means how often are the monies compounded. Withdrawals and

deposits are done at the start of each compounding period. Thus, if the

routine asks for a rate of interest, you might reply 12.5, meaning the

annual rate of interest is a 12.5 percent. If the rate is compounded

quarterly, then when asked how many periods, you would respond with 4. And

finally if you want to withdrawal or deposit $1,000 a year you would have to

divide this amount by four ($250) and enter that figure since there are four

periods per year. (SIDEKICK by Borland would be great for this calculation.)

At the end of each routine you are prompted with M(ain Menu) or

R(epeat)? Type M if you want to return to the main menu or type R if you

want to run another of the same calculations with different input. You must

return to the Main Menu to quit the program.

The following is a brief description of what each routine does:

Future Value of a Deposit

This routine will calculate the future value of a deposit. In other

word how much will a given amount be worth after a period of time when

invested at a given rate of interest.

Future Value of a Series

This routine is just like the one above accept that it assumes that

there is a series of deposits being made. That is, there are deposits being

made of a fixed amount at the start of each compounding period. These

deposits are made for the life of the investment. Example: Your IRA funds

are invested at a rate of 8.8 percent compounded quarterly. You want to

invest $2,000. each year for a period of 15 years. For this program you

must input $500.00 when ask for the deposit since it is assumed that the

deposit is made at each compounding period. The program will return to you

the value of the account after the 15 years assuming a deposit was made each

quarter.

Payment Required for Future Sum

This one is fun. You want to be worth a billon in 5.5 years! How much

do you have to deposit each compounding period at a particular rate of

interest to make it happen.

Present Value of Amount

Your Brother-In-Law owes you 100,000 big ones due in 7.2 years. He

offers to pay you $90,000 dollars today. This routine will tell you if it

is a good deal. You can throw the bum out if the present value exceeds the

90,000 that he is offering. On the other hand you can show your wife just

how dumb the guy is if the present value is less than $90,000.

Present Value of a Series

As above accept that the routine will tell you the present value of a

series of payments. Example: Your profit sharing may be drawn down in one

lump sum or you may accept a series of payments. Use this routine to tell

you which is the best way to go. If the present value is worth more than the

series of payments for the period, you'll know what to do.

Withdrawal of Funds

Congratulations! You just won the Publishers Clearing House's Grand

Prize of $125,00 and being a frugal person, you immediately run over to the

corner office of E. F. Hutton and deposit the funds in thier money market

accout. Now the question is, if you withdrawal a little bit every month,

how long will your prize last you? There will be no guessing with this

routine. This routine takes into account any interest rate, compounded for

any period and any size of withdrawal.

Interest Rate Earned

You held some stock for 3.75 years. When you bought it it was worth

$7,500 and when you sold it it returned, after commissions, $12,274. What is

the effective annual interest rate? If it is more that the average money

market rate for the period, pat yourself on the back.

Net Present Value, Uneven Cash Flow (NPV)

Very simple, if the result is positive, you have found an investment

that is returning your desired yield. If it is negative, it is not giving

you the return on your investment that you would hope to get. Routine asks

for amount invested and annual interest rate that you would LIKE to earn.

You then supply the cash flows that you expect. Each one can be different.

To stop entering cash flows, enter 0.

Time to Double

At a given rate of interest, at a particular rate of compounding how

long will it take for you to double your money.

Equivalent Interest Rate

CitiBank is offering 9.9 percent compounded daily. First Boston is

offering 9.5 percent compounded quarterly. Now just exactly who is giving

you the best deal? Run this routine to find out.

Straight-Line Depreciation

Computes an annual depreciation table using the above method.

Declining-Balance Depreciation

Computes an accelerated depreciation schedual and prints a table. Use

these table to help decide which is the best method to depreciate the office

computer.

Sum-of-Years-Digits Depreciation

Computes an accelerated depreciation schedual and prints a table. Use

these table to help decide which is the best method to depreciate the office

computer.

Break-Even Point

You are about ready to market the next best seller. This routine asks

you for your total of fixed costs. (Phone, Rent, Insurance etc.), Cost of

manufacturing the product (total cost of materials etc.) and the selling

price of the item. It then returns to you the number of units that must be

sold to break-even in your venture.

Economic Ordering Quantity (EOQ)

What is the most economical quantity to order for an item? Allows you

to input the overhead costs in processing an order. Then the routine takes

the total annual units of an item used and the unit carrying cost (interest

rate your funds earn multiplied by the purchase price for each unit) of the

item to calculate the most economical quantity to order. Buyers and Bosses

should love this one!

Sales Price with Discount

What is the total prices with tax for an item selling at a particular

discount?

Weighted Average

Calculates an average value for input of different values and amounts.

If you bought stock the first of each month at different prices and in

different quantities this routine will tell you what you paid in terms of

the average price per share. To stop entering values, enter 0 at a value

prompt. This routine will allow you to average up to 1,000 different values

and units. If you need it to allow for more inputs, contact the author!

Monthly Payment Calculation

Your in a fix and you need to borrow 10,000 from the local loan shark.

You can borrow the funds for 2.3 years at an annual rate of interest of 22.3

percent. What will your monthly payment be to the quy?

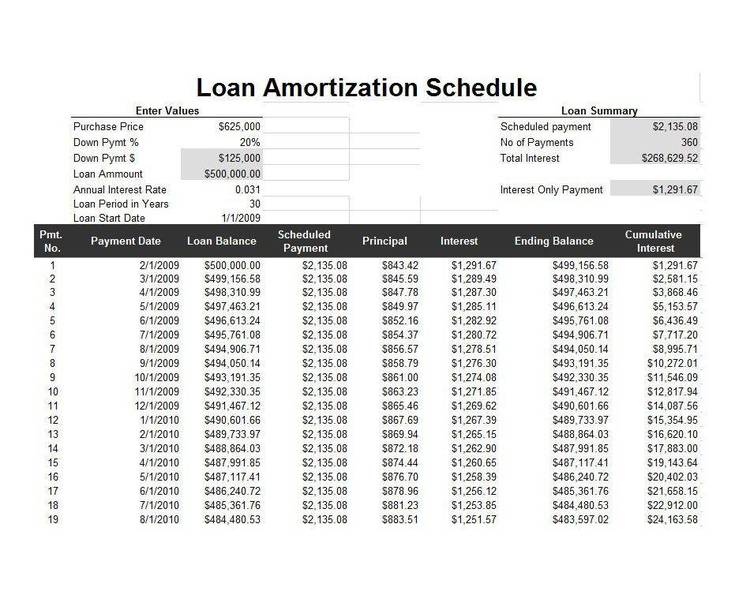

Mortgage Schedule

This will show you a loan schedule and what portion of any payment is

applied to interest and what part is applied to principal. You are asked

for the loan amount, interest rate, term of the loan, and the year for

which you want the table shown. At the end of the program you are prompted

with the usual M(ain Menu) and R(epeat) as well as A(other Year). The

difference between REPEAT and ANOTHER YEAR is that another year will use

the same loan conditions and just report back a table for a different year.

Repeat allows you to change the conditions of the loan. Note: you can see

a table for the twelve months following the 4.5 year mark, for example,

just by entering 4.5 when asked for what year. Also note, that when

prompted for the year the program will not allow you to enter a year

greater than the term of the loan. This routine can be used at tax time

when you need to see how much interest you paid on a loan.

Remaining Balance

Things are a little easier now and you want to pay off some loans.

This routine will show you what the balance is on a loan after any

particular payment.

Accelerated Payments

You were just promoted to head boss and with it you got a big fat

raise. Now you can pay an extra $125.00 toward the principal on your

mortgage. This routine will show you when your loan will be paid off and

how much interest you will save over the remainder of the loan. The

program prompts you for the terms of the loan (years, amount, & interest

rate) as well as the year of the increase and the extra amount paid. When

asked for year, DO NOT enter a year such as 1985, rather enter the year in

which the increase payments started, such as 3 for the third year or 9 for

the ninth year. Just for fun, assume you have a 30 year $75,000 mortgage

and you decide to pay and extra $75. per month after the fifth year. Take

a quess as to what year the loan will be paid off in and how much interest

you will save for the balance of the loan. Now run the routine and see how

close you came to the correct answer. Unless you are in finance, quaranteed

you will be suprised.

Balloon Payment

You are considering using one of the new "creative" ways to finance a

home. This calculates what the balloon payment is after a particular

number of years.

Affordable House Price

This will help you decide what mortgage you can afford. The routine

asks you for the annual interest rate on the loan, the length of the loan,

your annual income, an estimate of property taxes and insurance, the

percentage of your income for payments and the percentage you want to put

down. It will use these values to figure what you can afford when shopping

for a home.

Mortgage With Second

This will calculate the total monthly payment when carrying two

mortgages. It is assumed that only the interest on the second mortgage is

being paid.

Rental Property Analysis

If you are a land lord, or considering being one, this routine will

calculate your monthly cash flow from your rental property. The routine

considers your mortgage, annual interest rate, term of the loan, annual

insurance, taxes, & maintanence and the monthly income. (If you are a

renter, you could also figure out what your landlord is making off of you!)

I hope that these routines have some practical value for you.

Remember, if you find them of value please support my on going efforts to

supply user supported software by sending a contribution to the address

found on the title page of the program. If you use the software to create

or maintain income that such a contribution should be tax deductable.

Check with your account.

If you find these programs easy to use and you have a need to solve

other equations (engineers, financial advisers, researchers, etc.) contact

me so that we can explore the possibilities of encompassing your needs in

a similiar interface so that you can have a clerical person do a series of

calculations for you.

Karl Thompson

930 Wawaset Road

Kennett Square, Pa. 19348

December 13, 2017

Add comments